SMM February 6, 2025:

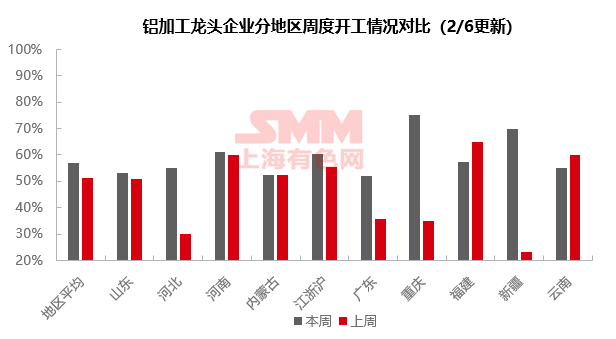

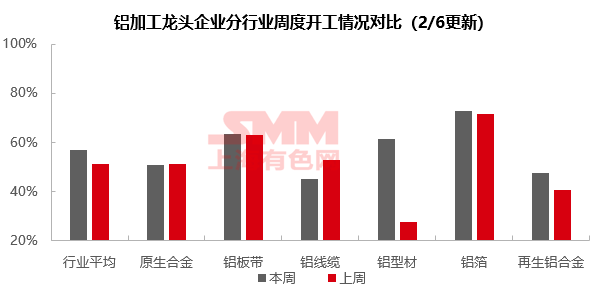

This week, the operating rate of leading downstream aluminum processing enterprises in China rebounded significantly, rising by 5.7 percentage points WoW to 56.8%, mainly driven by post-Chinese New Year holiday resumption of production. However, different sectors showed varied recovery trends. Specifically, aluminum plate/sheet and strip enterprises resumed work slowly, with only a slight increase in operating rates. High value-added products provided stable support, and a full recovery is expected after the Lantern Festival. The operating rate of aluminum extrusion enterprises rebounded to 61.3%, with leading industrial extrusion enterprises shortening their holiday, providing strong support for this week's operating rate. The aluminum foil sector saw its operating rate rise to 72.7%, driven by increasing orders and the initiation of overseas negotiations, with market expectations improving. The operating rate of secondary aluminum alloy producers rose significantly by 6.9 percentage points to 47.5%, but the delayed recovery of upstream and downstream sectors limited the speed of the rebound. Aluminum wire and cable, affected by weather conditions and reduced orders from the State Grid, saw its operating rate plunge by 8 percentage points to 45%, marking the largest decline among all sectors. The operating rate of primary aluminum alloy producers slightly decreased by 0.4 percentage points to 50.6%, as enterprises remained cautious in production during the off-season. It is expected to return to pre-holiday levels next week as downstream sectors recover. Overall, the residual effects of the Chinese New Year holiday are still evident, and a full recovery across all downstream aluminum sectors is anticipated after the Lantern Festival, with operating rates expected to maintain an upward trend. According to SMM forecasts, the operating rate of leading downstream aluminum processing enterprises in China is expected to rise by 3.9 percentage points to 60.6% next week.

Primary Aluminum Alloy: This week, the operating rate of leading primary aluminum alloy enterprises in China recorded 50.6%, down 0.4 percentage points compared to the last week before the holiday. As more than half of the enterprises maintained normal production during the Chinese New Year holiday, the post-holiday operating performance in the first week showed little difference from the last pre-holiday week. Some enterprises even saw a slight increase in operating rates, performing relatively well. However, February is generally an off-season for the primary aluminum alloy sector, with some producers adopting a wait-and-see approach and maintaining a slow production pace. As downstream sectors enter the post-holiday recovery phase next week, demand is expected to improve, and the operating rate of primary aluminum alloy producers may return to levels near the pre-holiday norm.

Aluminum Plate/Sheet and Strip: This week, the operating rate of leading aluminum plate/sheet and strip enterprises slightly increased by 0.4 percentage points to 63.4%. As the first week after the Chinese New Year holiday, the resumption of work in aluminum plate/sheet and strip enterprises was relatively slow. Apart from high value-added products such as automotive and aerospace plates, which were less affected by the holiday and maintained relatively stable orders, demand for other products from downstream sectors still needs to recover. With the Lantern Festival marking the end of the holiday period next week, demand is expected to pick up, and the operating rate of aluminum plate/sheet and strip enterprises may return to pre-holiday levels.

Aluminum Wire and Cable: This week, the operating rate of leading aluminum wire and cable enterprises in China recorded 45%, down 8 percentage points WoW. According to SMM, leading aluminum wire and cable enterprises gradually resumed work after the sixth day of the Chinese New Year, and most enterprises have now resumed normal production, proceeding with their production schedules as planned. However, unfavorable weather conditions at power grid construction sites and lower bidding amounts for aluminum wire and cable in 2024 compared to 2023 have slowed the post-holiday delivery process for State Grid orders, resulting in weaker operating performance compared to the same period last year. SMM believes that the aluminum wire and cable sector has been significantly impacted by the Chinese New Year holiday in the short term, but operating rates are expected to rebound to some extent in the coming weeks.

Aluminum Extrusion: This week, the overall operating rate of the domestic aluminum extrusion sector reached 61.3%, showing a significant rebound compared to the previous period. Among the sub-sectors, industrial extrusion performed particularly well, with some leading automotive extrusion enterprises shortening their holiday, providing strong support for this week's operating rate. PV extrusion enterprises maintained stable operations with no new orders, mainly due to the lack of significant recovery in downstream component production schedules. In the construction extrusion sector, leading enterprises resumed work in an orderly manner after the holiday. A full recovery in the aluminum extrusion sector is expected after the Lantern Festival, as some small and medium-sized plants are still on holiday. SMM will continue to monitor post-holiday production resumption and order recovery trends. (Note: Some sample enterprises for leading enterprises have been updated starting this week.)

Aluminum Foil: This week, the operating rate of leading aluminum foil enterprises rose by 1.3 percentage points to 72.7%. Following the end of the Chinese New Year holiday, most downstream customers of aluminum foil plants have resumed production, leading to a gradual increase in orders for aluminum foil enterprises and boosting the operating rates of some leading enterprises. Some aluminum foil products are about to enter new annual overseas market long-term order price negotiations, which may impact the subsequent operating rates of aluminum foil enterprises. Meanwhile, the actual stimulating effects of national subsidy policies on end-user markets such as automotive and home appliances should not be overlooked and require continuous attention.

Secondary Aluminum Alloy: This week, the operating rate of leading secondary aluminum enterprises rose by 6.9 percentage points to 47.5%, mainly driven by post-holiday resumption of production. Large secondary aluminum plants or enterprises supplying liquid aluminum directly resumed production earlier, between January 31 and February 5, while other enterprises gradually resumed production between February 6 and February 9. As a result, the operating rate of the sector has rebounded significantly this week, but it is expected to gradually return to normal levels next week. However, the recovery on the demand side has been relatively slow. Although secondary aluminum enterprises have resumed operations on the sales side, insufficient downstream activity has kept the overall market atmosphere subdued. The operating rate of secondary aluminum producers is expected to maintain an upward trend next week.

Click here to view the SMM Aluminum Industry Chain Database

(SMM Aluminum Team)